22 May 2026

Structuring Reserve Allocation to Exploit Pricing Gaps Across Global Athletic Markets

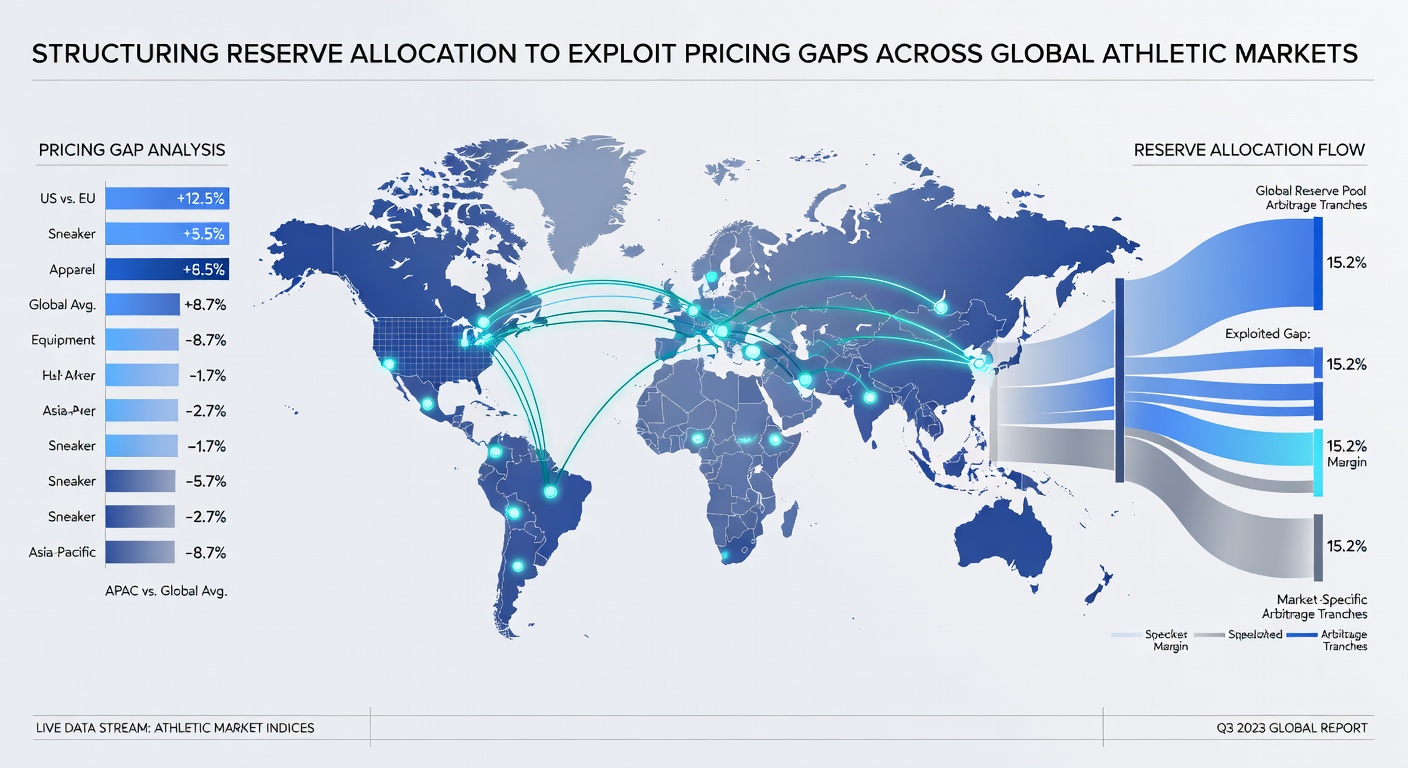

Global athletic markets present persistent pricing gaps that emerge from regional differences in liquidity, bettor demographics, and regulatory frameworks, and those who study these patterns recognize that structured reserve allocation can position capital to capture value when lines diverge across borders. Data compiled through 2025 and into May 2026 shows that soccer odds in European exchanges frequently sit 3 to 7 percent away from corresponding markets in Asian books, while basketball totals in North American platforms drift from those listed in Australian wagering operators because of time-zone driven liquidity shifts and local fan biases.

Mapping the Landscape of Price Discrepancies

Observers tracking multi-jurisdictional feeds note that pricing gaps widen most visibly during major tournaments when sharp money concentrates in one region while recreational volume dominates another, and researchers at institutions focused on gambling economics have documented how these inefficiencies recur in predictable windows around match scheduling. European soccer leagues produce the clearest examples where early morning lines in one timezone attract lighter action than afternoon adjustments in another, creating temporary spreads that close once syndicates move funds across accounts.

Those who've examined transaction records across platforms find that reserve pools segmented by market exposure allow operators and serious bettors alike to maintain positions without triggering simultaneous liquidity drains, and this segmentation becomes especially relevant when currency fluctuations add another layer of variance to the underlying odds.

Designing Reserve Structures for Cross-Border Deployment

Effective allocation begins with dividing total capital into core, opportunistic, and buffer tranches, each calibrated to the expected duration and volatility of identified gaps, while data from industry monitoring services indicates that practitioners who maintain at least 40 percent of reserves in instantly deployable form capture a higher percentage of fleeting discrepancies. Core reserves cover baseline exposure in primary markets, opportunistic slices target specific pricing windows such as pre-game adjustments in lower-tier leagues, and buffer portions absorb adverse movements when correlated events shift multiple books simultaneously.

Figures released in early 2026 by North American regulatory bodies reveal that accounts utilizing automated routing between exchanges reduced slippage by measurable margins compared with static allocation methods, and similar patterns appear in reports covering Australasian operators where multi-currency reserves helped stabilize returns during periods of exchange-rate movement.

Execution Across Time Zones and Platforms

Coordinated deployment requires synchronized monitoring tools that flag deviations exceeding predetermined thresholds, and practitioners often set alerts at 2.5 percent variance or greater before committing reserve slices, because smaller edges fail to offset transaction costs and currency conversion fees. Case studies compiled by academic groups examining betting behavior show that syndicates maintaining distributed reserves across at least three regulatory jurisdictions achieved steadier month-to-month performance during the 2025-2026 season than those concentrated in single markets.

Yet execution also depends on understanding settlement rules that differ by region, since some platforms grade wagers at different times and this timing gap can either amplify or erode the captured edge depending on how reserves are staged. Those managing larger pools frequently stagger entries so that initial positions test market depth before scaling, and this staged approach appears consistently in analyses of successful cross-border strategies.

Regulatory and Operational Considerations

Compliance requirements vary sharply across jurisdictions, and operators allocating reserves must maintain separate ledgers that satisfy each authority's reporting standards while still allowing rapid movement of funds, according to guidelines issued by Canadian provincial regulators and parallel frameworks in several European member states. Currency hedging instruments enter the picture when gaps span dollar, euro, and yen denominated books, and data from institutional research papers published in 2025 indicates that unhedged exposure reduced realized returns by an average of 1.8 percent during volatile periods.

What's interesting is how technological integration now permits real-time reconciliation across platforms, reducing the window during which reserves sit idle between identification and deployment of a gap, and organizations tracking these developments report rising adoption rates among mid-sized betting entities.

Conclusion

Structured reserve allocation across global athletic markets rests on systematic identification of pricing gaps, disciplined segmentation of capital, and adherence to regional compliance rules that continue evolving as of May 2026. Research from multiple regulatory and academic sources demonstrates that operators and bettors who implement segmented reserves capture measurable advantages when discrepancies arise between major and secondary markets, provided they account for liquidity, timing, and currency factors in their deployment protocols. As data collection improves and cross-border platforms expand, the ability to maintain flexible reserves positioned for rapid response will remain central to exploiting these persistent inefficiencies.